This is a curated set of my Linkedin posts going back to late 2022. I’ve been posting more stuff there recently and of course not everyone’s on it so many won’t see them.

I think Linkedin’s great at showing us new stuff, but not so great at helping you find older stuff if you haven’t bookmarked it.

For longer, more in depth posts I’ll always publish them on my blog or as articles in Marketing Week.

But for Linkedin posts (which are naturally more bitesize) I’ll add new ones to the top of this post.

10.10.24 – CATHERINE KEHOE’S SPEECH AT THE IPA EFFECTIVENESS AWARDS DINNER

On Monday night at the IPA Effectiveness Awards, Catherine Kehoe, Chief Customer Officer of Nationwide, delivered what I can only describe as a sermon to modern day effectiveness, to a hushed room of hundreds of rarely silenced ad people.

Everyone should read the full text, link below. But this section chimed especially strongly with me:

‘We have entered a new era of marketing effectiveness, but still much of our thinking has been honed from the age of ‘air power’, that saw carpet bombing and surgical strikes managed from a central command post…

But this is going in reverse now. The growing weakness of TV as a mass reach and mass event medium is well documented…

And so, we are increasingly entering in a world of brands being built on the ground, by armies of influencers, by brand partnerships and collaborations, and by in-feed and in-game activations. Hand-to-hand marketing is replacing fire-and-forget…

And there’s no way any of us can keep up unless we work together.”

Here’s to this new era of marketing effectiveness.

https://lnkd.in/eExKG-Zr

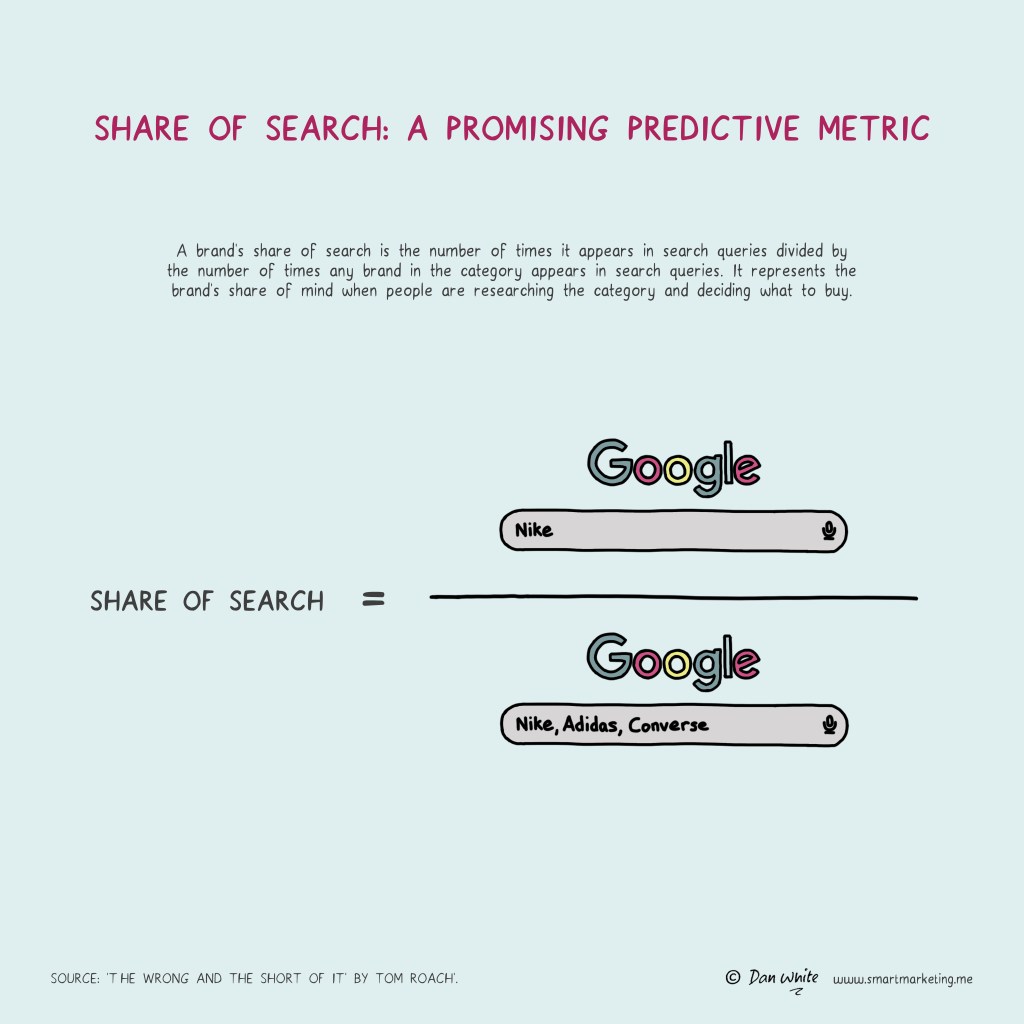

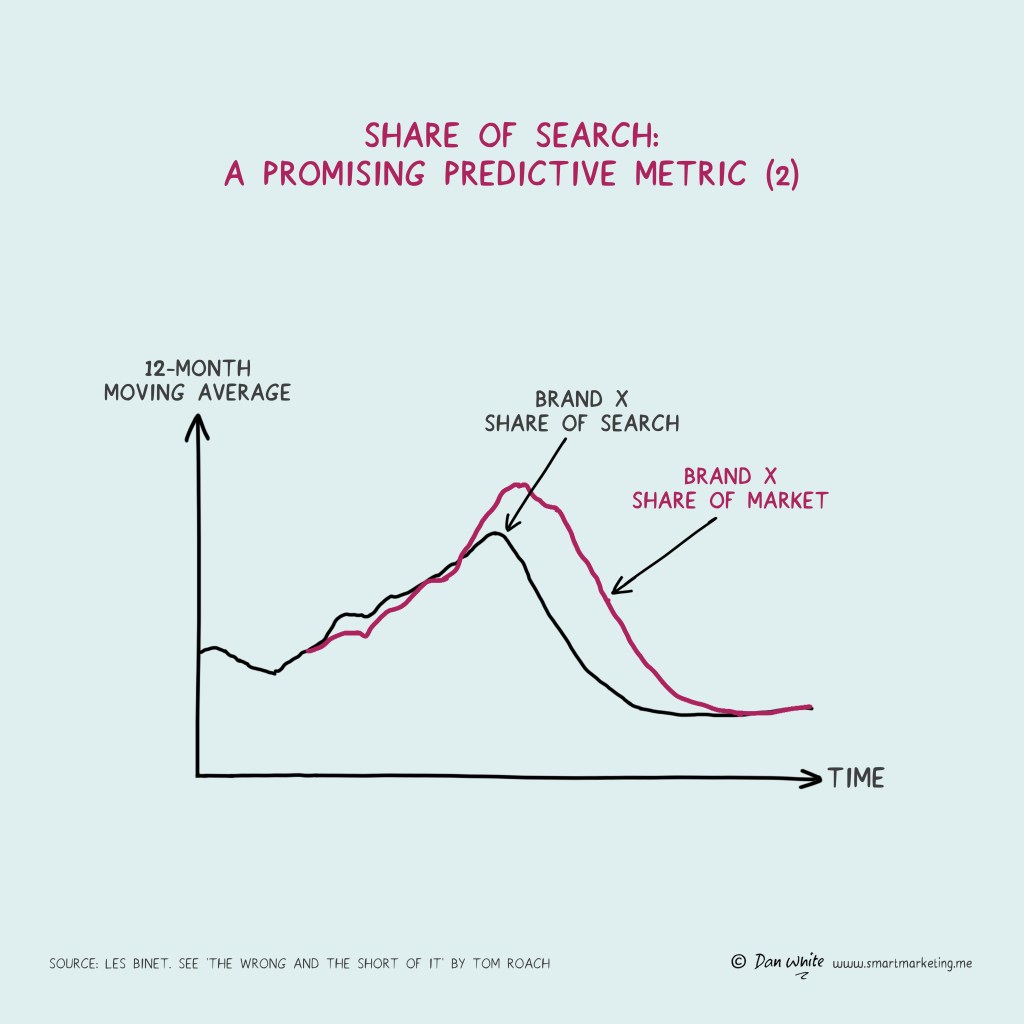

4.10.24 – THERE’S A NEW ‘SHARE OF’ IN TOWN

A few months ago we* had an idea.

Given the massive growth of LLMs, the fact that their training data mirrors how brands are thought of in the real world, and that they’re becoming places people turn to for recommendations…wouldn’t it be helpful if there was a simple, reliable way for marketers to understand how LLMs think about their brands?

So we built the Share of Model™ platform – to understand what AIs are saying about your brand. You can get a flavour of the platform and early access here: https://shareofmodel.ai/

Link to the original Marketing Week article about all this in the comments, including some history on some of the other ‘share ofs’ – share of market, share of voice, share of search.

Jellyfish, The Brandtech Group, Benjamin Pipat, *actually Jack Smyth

hashtag#marketing hashtag#AI hashtag#GenAI hashtag#brands

25.8.24 – INVITATION TO MARK RITSON TO JUDGE THE APG CREATIVE STRATEGY AWARDS 2025

The great Mark Ritson recently wrote a brief but provocative post about hating the title ‘creative strategist’.

On behalf of the APG, the home of planners and strategists, this is an invitation for Mark to come and judge the APG’s Creative Strategy Awards 2025.

His post posed tough questions for anyone whose job is or includes creative strategy. It received 1000+ likes and a huge amount of agreement.

The essence of it was that the title is an oxymoron – that you can’t be both an expert strategist and an expert creative. Mark is rightly a purist when it comes to strategy. To him the title wrongly blurs the lines between two things which should be distinct.

APG members are a broad church and whilst most aren’t creative strategists by job title, many will see creative strategy as part of their role, and naturally the APG feels some responsibility to stand up for the value creative strategy has, especially the discipline and the process, perhaps more than the title.

Over the years I’ve been an account planner, brand planner, strategist, brand strategist. This job has a proud history going back to when two 70s legends, JWT’s Stephen King and BMP’s Stanley Pollitt, jointly invented account planning. The changing nature of the role, including its recent sub-variant creative strategy, tells a story of the evolution of advertising. All these titles are flawed.

And whilst I’m not a creative strategist by title, his post hit a nerve for me for three reasons.

First, many people who are planners or strategists like me, wear a ‘creative strategy’ hat part of the time. This part of the job is about working closely with creative people to help make impactful creative work that executes a brand’s marketing communications strategy. Is this strategy? Or creativity? It’s true the label doesn’t fit the proper delineation between strategy and execution.

Second, I work closely with some brilliant people called creative strategists at Jellyfish, strategically-minded creative thinkers who are experts in getting the best out of social platforms. I see the value they bring to our clients every day.

Third, because of the fantastic non-profit organisation the APG, whose committee I sit on, and whose Creative Strategy Awards I’m hugely proud to have been asked to chair in 2025.

We’re not going to try to persuade Mark it’s a perfect job title, but we would like him to see, read and discuss with us the very best of this thing called ‘creative strategy’ being done by people with all sorts of job titles across the world today.

All the APG asks is that you consider our invitation, Mark. Final round judging takes two days in London in July ’25. We’ll put aside any differences on the name, but would love to debate the merits of the work.

For a look at the winners from 2023, including the phenomenal Grand Prix winning ‘Raise your arches’ by Leo Burnett London for McDonald’s, visit https://lnkd.in/ef7uTXY9

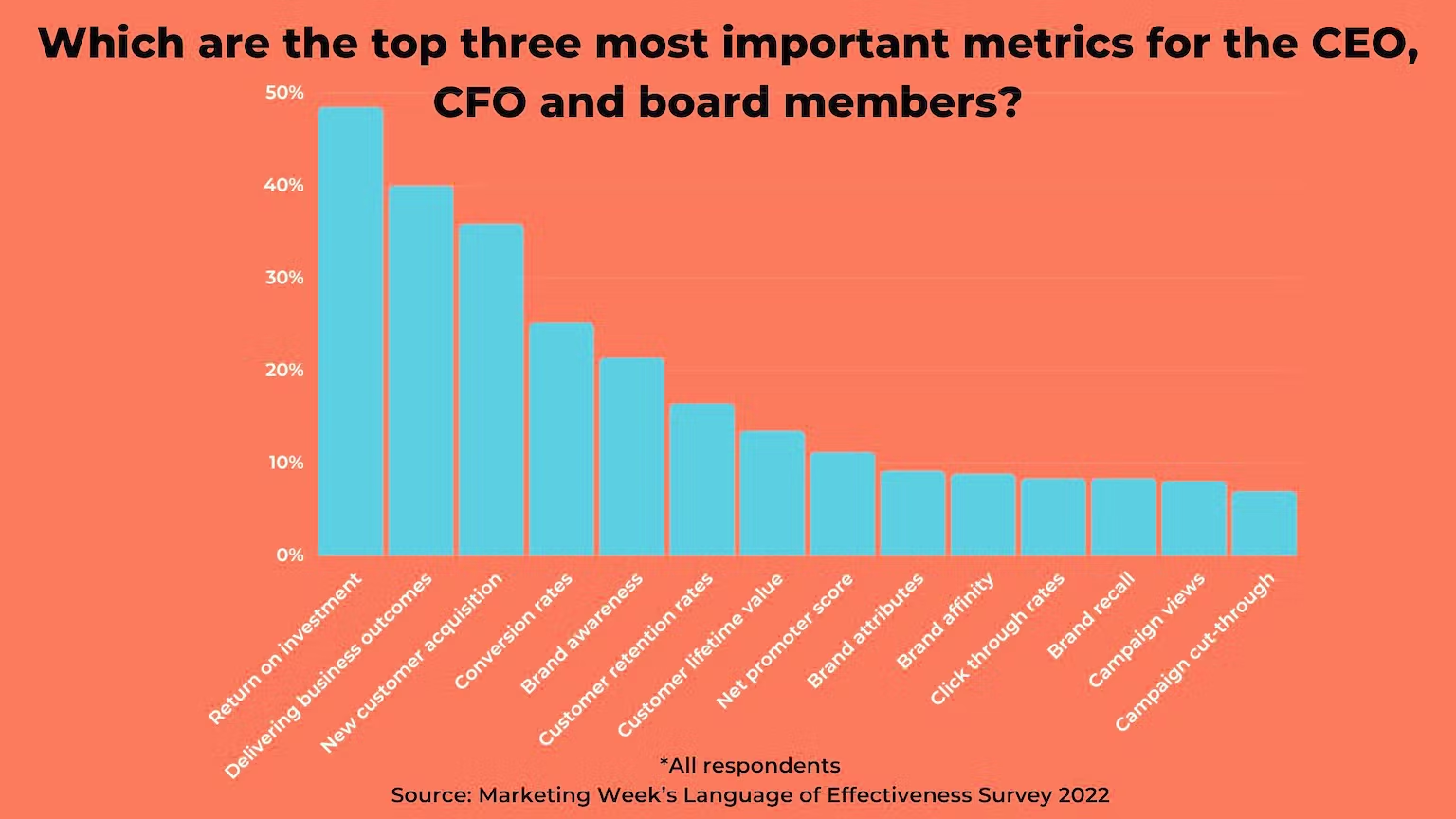

21.6.24 – THE METRICS THAT MATTER, TO THE BOARD

Notes from my Cannes panel on getting the C-Suite to value creativity

There can be no creative marketing unless businesses will pay for it. That means getting decision-makers to value it.

Which means finding objective ways to measure it.

Cannes is a great reminder that creativity can be slippery, unpredictable, hard to define, highly subjective.

And that’s a challenge. Because the people we need to persuade to invest in it, prize objectivity above all.

They will only invest resources in things that will result in tangible, visible improvements in their businesses.

On Wednesday I facilitated a discussion hosted by CreativeX on ‘The metrics that matter, to the board’ with some brilliant panellists, Joanna Stringer (Boston Consulting Group (BCG)), Brigitte King (Colgate-Palmolive), and Susan Jones (Diageo).

Here’s a summary of the conversation:

There was strong consensus around the contribution of brand creativity to commercial value today. Yes there’s work to be done persuading tech businesses on this, but the big ones get it – Amazon, Google, Apple. The brand era isn’t dead, Prof G.

The challenge now is less about proving brands and creativity can create value, and more about improving the value they create.

We’re in a 3rd age of effectiveness. Not purely brand, or an age myopically-obsessed with granular performance metrics. But an age when we win by combining long-term brand efforts with short-term performance efforts.

In this era, brands will get and stay big via a collection of smalls – simultaneously reaching and finding relevance with multiple audiences in a highly fragmented media ecosystem.

Platforms and algorithms are the new gatekeepers to success. Our creative work needs to be made both for people and algorithms to drive maximum impact.

But a gap has opened up between the small number of assets we’d ideally create and the vast quantity of assets the platforms demand that we create.

This all creates challenges in how we elevate the value of creativity to the C-Suite.

We now need creative metrics that scale – brands are deploying thousands of assets. It’s no longer enough to pre-test one execution and believe the score is representative of the value you’ll create. AI is our friend here.

We need metrics that can ensure our work is ‘fit for platform’, a fundamental driver of effectiveness today. CreativeX’s creative quality score (CQS) is used by both Diageo and Colgate-Palmolive to ensure they’re able to continuously improve their creative and its deployment in a way that’s easy to grasp and report in an objective way.

But ensuring fitness for platform is not enough.

We now need a true measure of creative excellence that can prove the added value we’re creating for brands. It needs to scale, be objective, and be a practical lever to help us make our work better. AI will be our friend here too.

That’s the next frontier in proving the value of creativity. Let us know if you think you’ve got the answer.

Original Linkedin post: https://www.linkedin.com/posts/tom-roach-5b468026_there-can-be-no-creative-marketing-unless-activity-7209855666285379584-mDJ-?utm_source=share&utm_medium=member_desktop

21.6.24 – PSA TO THE CLIENT COMMUNITY ON WRITING BETTER BRIEFS

This is a PSA from the agency world to everyone in the client community.

Cannes is done. Hundreds of awards have been handed out.

Whether there or not, whether inspired by the creativity on display, infuriated by it, unmoved by it, or even completely oblivious to it, everyone in marketing should be able to agree on this: we can all make better creative work.

Whether that means raising your floor or raising your ceiling.

But the start point isn’t on your agencies or your inhouse teams.

It’s on you. It has to start with your strategy and your brief.

The truth is, most briefs aren’t great. In fact most briefs aren’t briefs at all. Sometimes they’re just a call, or worse, just a WhatsApp.

Sometimes agencies are even expected to telepathically intuit that a brief even exists.

Whatever your situation or aspiration, we can all agree that we could do with better briefs.

Some friends have a startup aiming to help solve this problem and have spent a year developing a platform working with real clients.

Their mission is that everyone should be able to write a great brief. And they’ve built a self-serve platform, a sort of Grammarly for marketing briefs, to help.

I’ve had early access and think it looks quite cool. And they’re giving everyone 10 days free access to make it easy for everyone to try. (Apparently not yet optimised for mobile so if you want to sign up try it on a laptop).

Not everyone can get a Cannes Lion. But everyone can write better briefs.

Original Linkedin post:

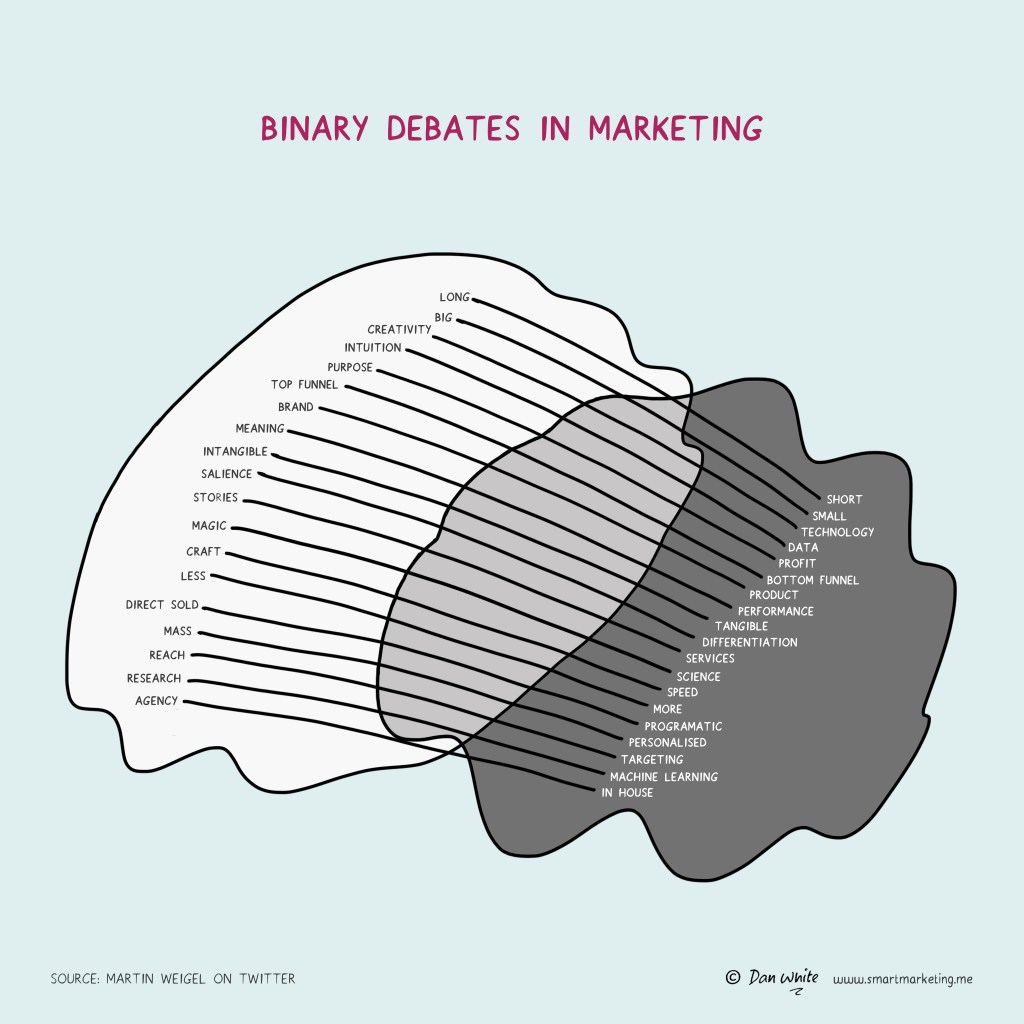

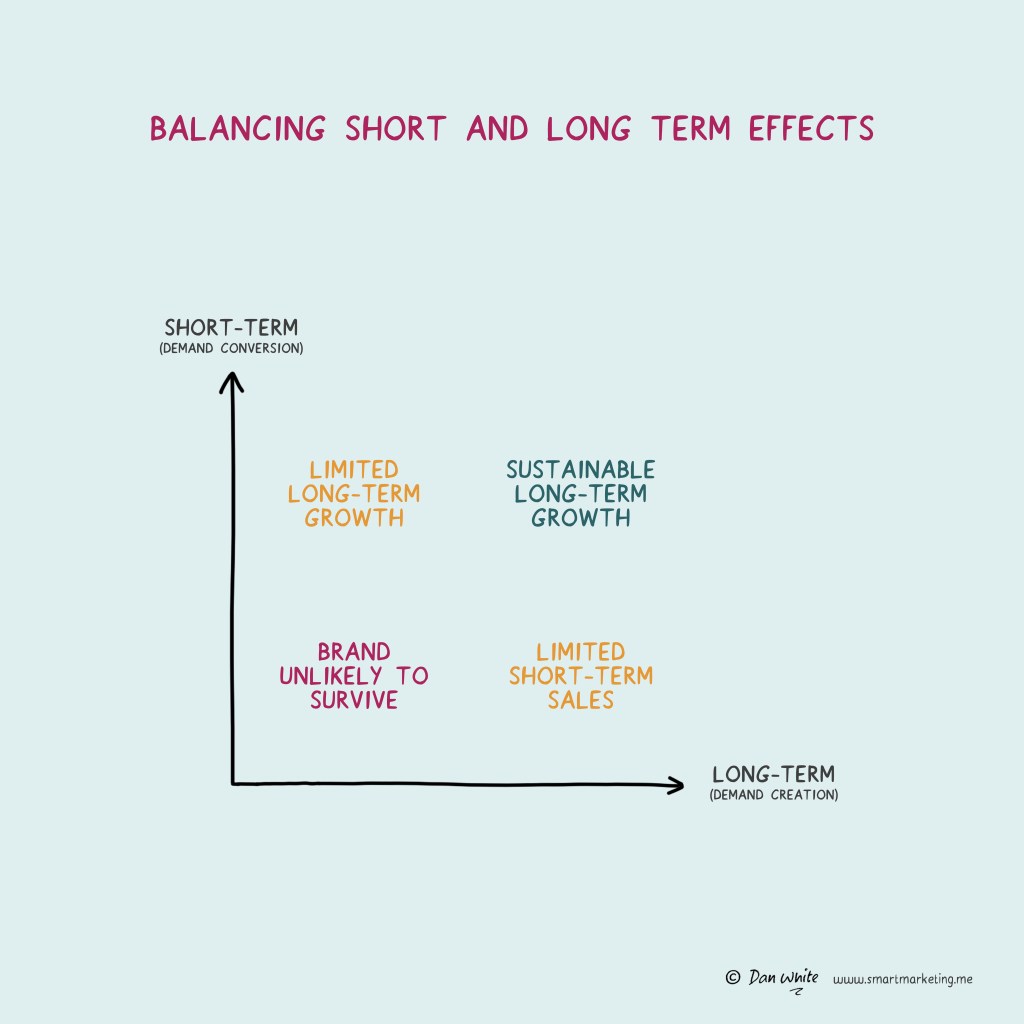

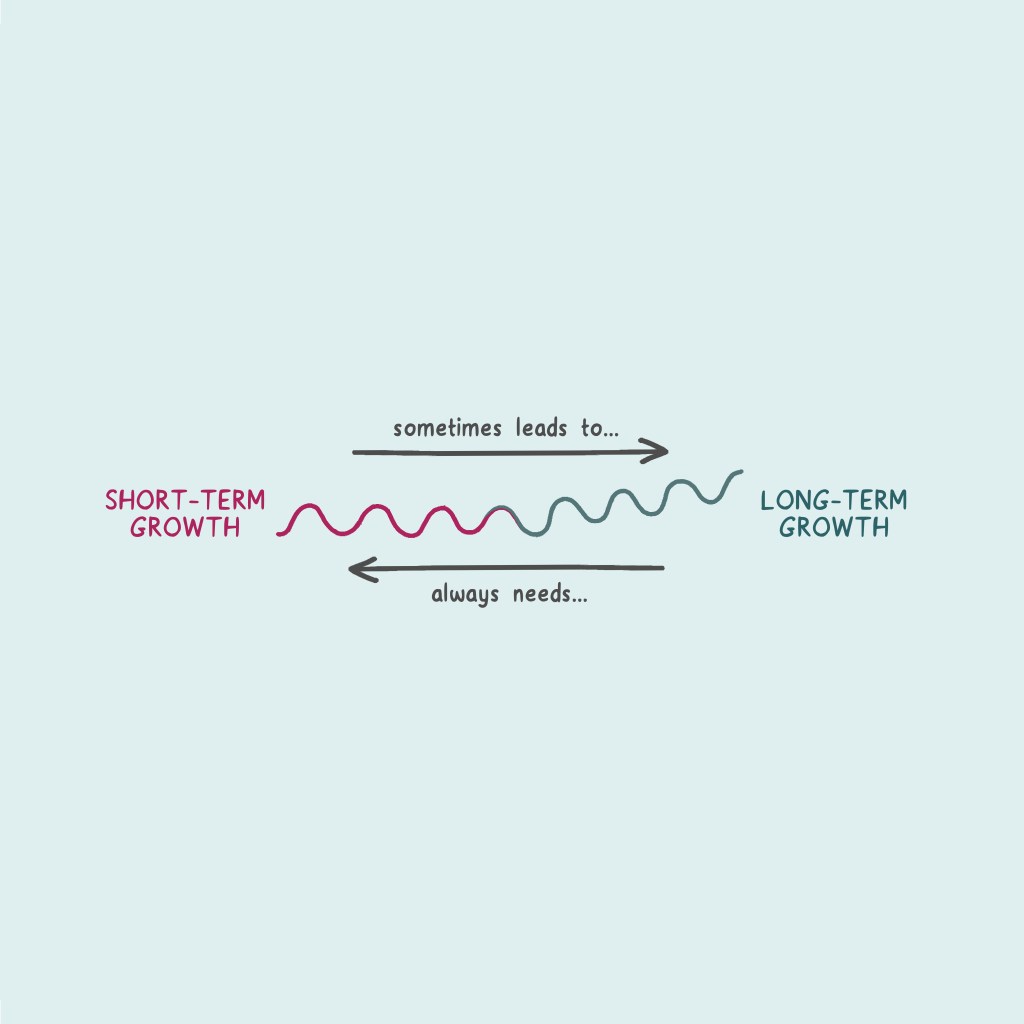

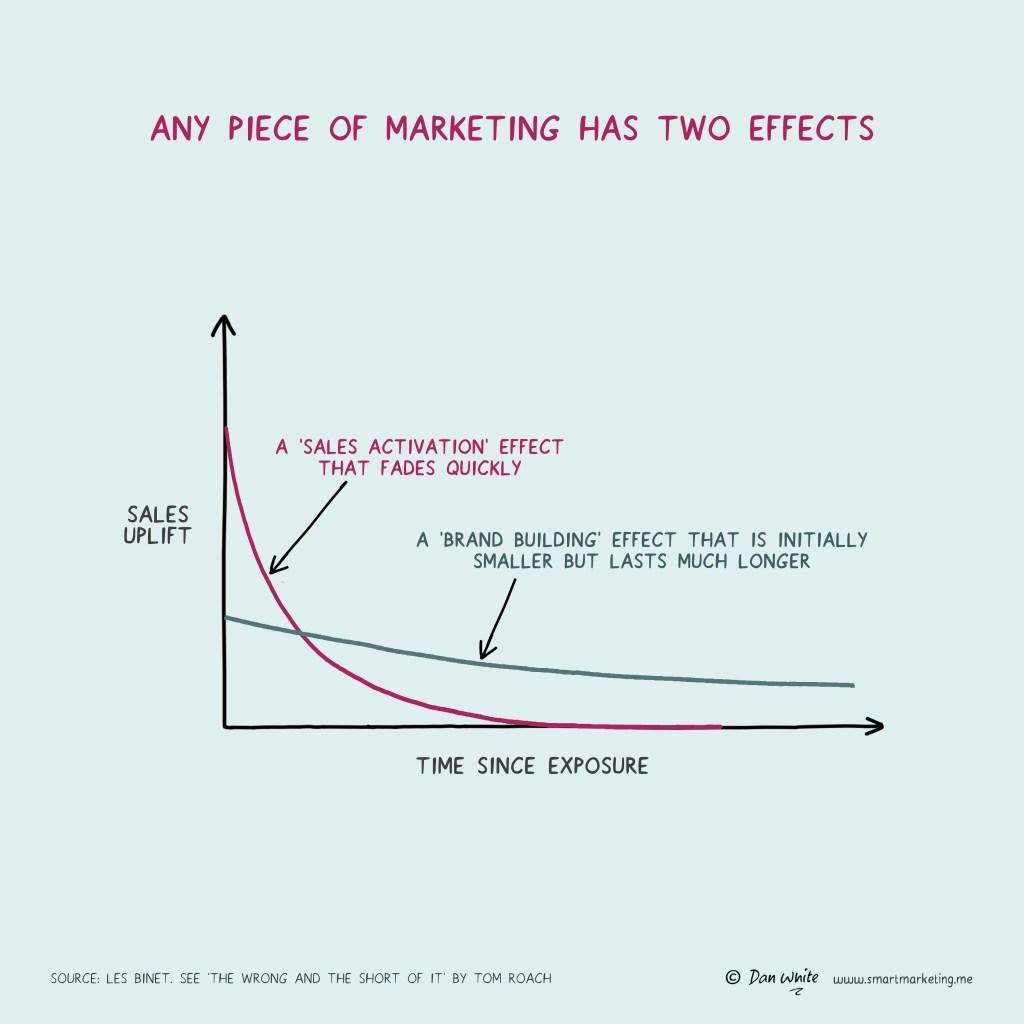

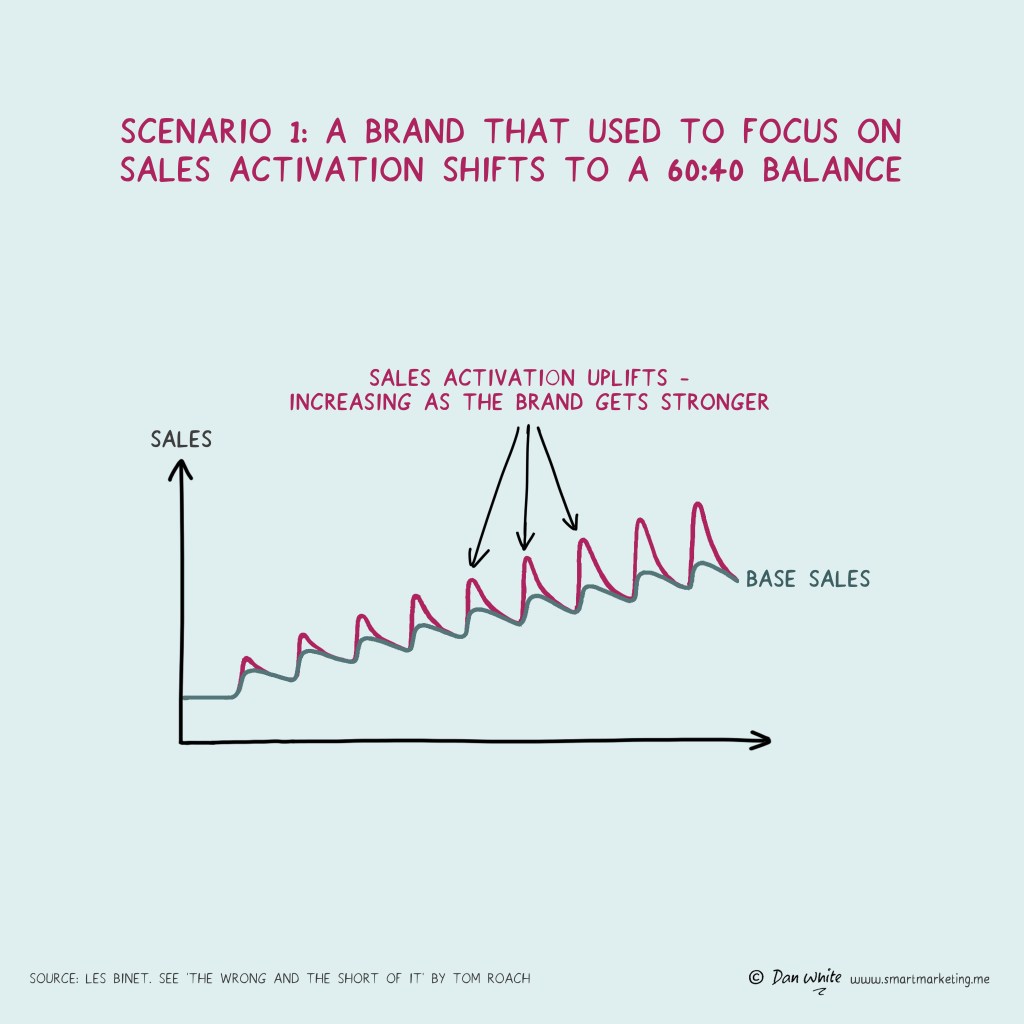

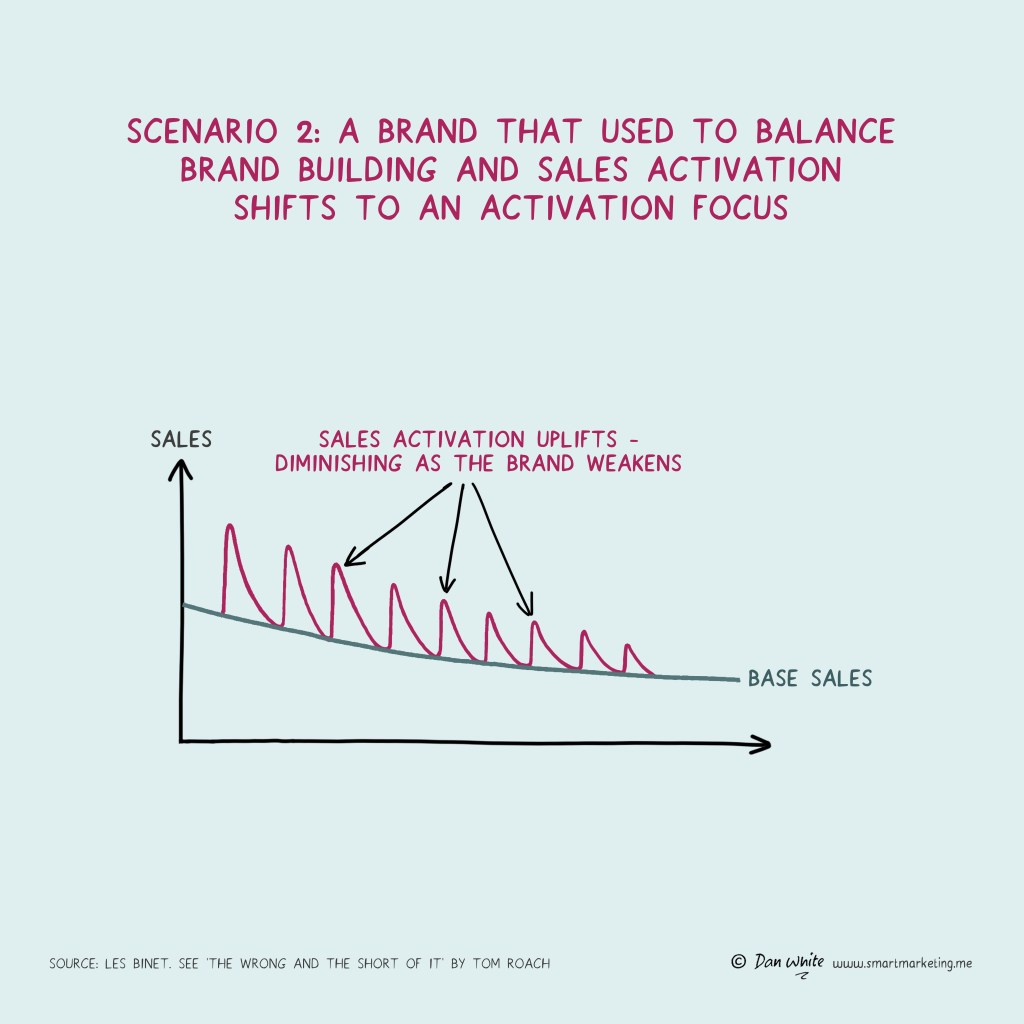

15.6.24 – THE WRONG AND THE SHORT OF IT…AGAIN

[On re-publishing a slightly updated version of a 4-year old blog post]

Four years ago I published my first ever article on my brand new blog.

70k+ reads later it’s still my most popular post.

It was called ‘The Wrong and the Short of it’ and was a rallying cry for us to end the dumb division between brand and performance marketing and the false choice between long and short term marketing tactics. Someone commented that the marketing philosophy contained in it should be called ‘bothism’, a label which seems to have stuck.

I especially love it when it gets read and shared by people who weren’t previously familiar with the work of the big names in marketing effectiveness from the UK/Aus/NZ, especially US performance marketing people, and they develop a taste for the work of Binet & Field and others as a result.

My reason for re-publishing it and sharing it here is that the brilliant marketing author and illustrator Dan White has kindly created a new set of illustrations for it which have given it a nice new look.

So if you know marketers struggling with the limitations of short term tactics, with brands that are stuck on the performance plateau, or with leaderships who ‘don’t get brand’, who might benefit from reading this, please do pass it on.

Or please do drop me a line as I work at a company, Jellyfish, part of The Brandtech Group, which is uniquely set up to bridge a range of divides across marketing – whether that’s brand & performance, media & content, data & creativity, and marketing’s latest false dichotomy, GenAI & humanity.

Original Linkedin post:

7.6.24 – IPSOS REPORT ON USING TIKTOK THROUGH THE FUNNEL

[Commentary on new research report by Ipsos on TikTok]

Many brands are all over the place in terms of how their paid ads and organic content sit alongside each other. Brands need to get them working better together, remove the silos, and think ‘one social’.

Paid ads can get you reach, but tend to be less like what people are there to watch. Organic content fits better with what people want to watch, but is often inconsistent in terms of reach, or too poorly branded, to make an impact on the brand.

It’s why so much of the advertising effectiveness research suggests that ads and content need to be ‘fit for platform’ or ideally platform-native to start with.

You need to work out how to get the ‘best of both’.

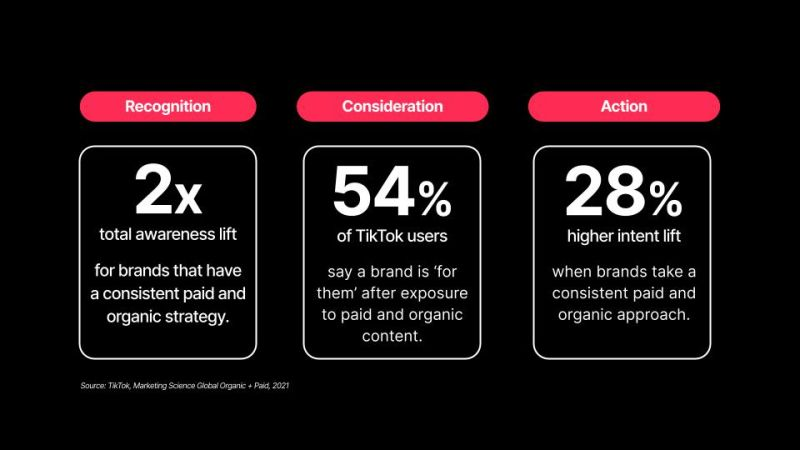

So it’s interesting to see TikTok thinking about how paid and organic can work in harmony and be planned together better through the funnel (new report, link in comments).

Summary including link to download report https://www.tiktok.com/business/en-SG/blog/missions-for-the-modern-marketer

Original Linkedin post:

5.6.24 – PRACTICES CHANGE, PRINCIPLES ENDURE

[Commentary on new research report by Ipsos on TikTok]

Practices change, principles endure.

So it’s always fascinating to see platforms arrive on the scene and change advertising practice, but later embrace some of the fundamental principles of brand building as they mature as more rounded advertising platforms.

New report here from TikTok and Ipsos suggests they’re embracing some of the fundamentals – that brands grow by attracting new users; that you need to capture future demand, not just convert existing demand; that you need to build long-term brand memories by being consistently distinctive over time.

But also includes practical advice around tailoring content to platforms, combining the strengths of paid ads and organic content, and using organic as a playground to help you get your paid ads working more effectively.

And some useful case studies especially relevant for APAC teams.

Summary and link to full report here:

https://www.tiktok.com/business/en-SG/blog/missions-for-the-modern-marketer

Original Linkedin post:

27.5.24 – MARKETING TRAINING

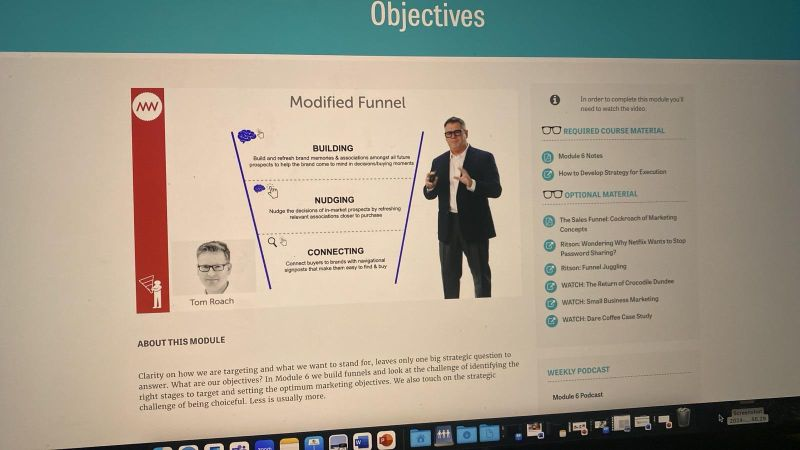

Whenever one of Mark Ritson’s great MiniMBA in marketing courses is running, people I know who are on them send me messages pointing out that an article of mine is on the reading list.

Last week a couple of different people sent me this image. (I was actually a bit surprised as I thought Mark hated my piece on the sales funnel, as he thinks, as I also do actually, that in an ideal world you’d build your own bespoke funnel rather than using an off the shelf framework).

Anyway, the sheer number of people I now know who’ve taken his courses got me thinking that there’s recently been somewhat of a quiet revolution in marketing training, especially online, that’s gone mostly unremarked.

It’s long been an issue that unlike in other disciplines, marketers don’t get the professional training they need, and that this holds everyone back, stopping them from earning the respect they deserve.

But what hasn’t really been talked about much is the breadth of great courses now available that are helping solve the problem.

The huge success of Ritson’s courses opened the floodgates, and now many of the big names in marketing effectiveness have got their own courses.

Grace Kite & Magic Works on marketing effectiveness; Cannes Lions and 42 Courses have content from gurus like Rory Sutherland, Les Binet & Peter Field; James Hurman on ad effectiveness; John Hegarty on creativity; Scott Galloway on brand strategy (surprising for someone who thinks ‘the brand era is dead’).

All with the result that the marketing world is now especially well served if you or your team needs training in classic marketing strategy, brand marketing or ad effectiveness.

But marketing today is an incredibly broad church.

Like it or not (and I know many will say not), marketing has got phenomenally complex. There’s now a huge array of roles that are technical and specialist. And even people in non-technical roles need a broad understanding of a wide range of disciplines.

So whilst there’s loads of highly credible training out there covering the big strategic stuff, there still seems to be far less quality training out there on the specialist stuff – big and small – that’s needed to deliver it in practice.

Which brings me onto Jellyfish. When I arrived I couldn’t believe how different it is to the network agencies. And one of things that is most different, but is still fairly unknown, is that we’ve got a global training arm set up to train marketers (including our clients and partners at the major platforms too) in how to use pretty much every part of the modern marketing toolkit. (Link in comments if you want to check out the full range of courses available).

With all the great training now out there, it will be fascinating to see if over time this is going to help marketers earn the respect they deserve.

Original Linkedin post:

26.5.24 – DAVE DYE’S PODCAST WITH PAUL FELDWICK

Wonderful conversation between two ad legends. So much wisdom here.

Especially good on the development of the famous Rowan Atkinson Barclaycard campaign. Including the brilliant ‘insight’ that led to that campaign that was ‘people quite like Rowan Atkinson and find him funny’.

It’s permission for anyone who ever feels pressure in their work to come up with a perfect insight in the form of a ‘revelatory truth’, that it probably isn’t necessary or worth the effort. But a reminder that understanding your audience always is.

So listen to this, subscribe to Dave Dye’s blog/cast ‘Stuff from the loft’, and read Paul’s books (both ‘Why does the peddlar sing?’ and ‘The anatomy of humbug’).

Do this not for the nostalgia but for what it can teach us about making better advertising today.

Original Linkedin post:

28.3.24 – THE IPA EFFECTIVENESS AWARDS – THE GOLD STANDARD BUT THEY MUST EXPLORE NEW FRONTIERS

The IPA Effectiveness Awards have been the gold standard in advertising effectiveness for over four decades. No advertising awards scheme comes close in terms of their value to the industry. But to maintain relevance it’s vital that it explores new frontiers, and doesn’t just reward the usual suspects. More on this in my WARC article below.

So am really proud to be an industry judge this year alongside my Jellyfish colleague Di Wu, VP of Data Science, who’s on the technical judging panel. As an actual ex-NASA scientist she knows a thing or two about new frontiers.

Original Linkedin post:

24.1.24 – GenAI isn’t marketing’s future, it’s already part of marketing’s present

Latest from me in Marketing Week is a rundown of some of the many ways GenAI and AI are changing the way we work in marketing today.

Includes a broad range of companies doing interesting things across segmentation, research, insights, briefing, strategy, creative development, production and measurement. (And the first outing for my digital twin, TomAI).

Original Linkedin post:

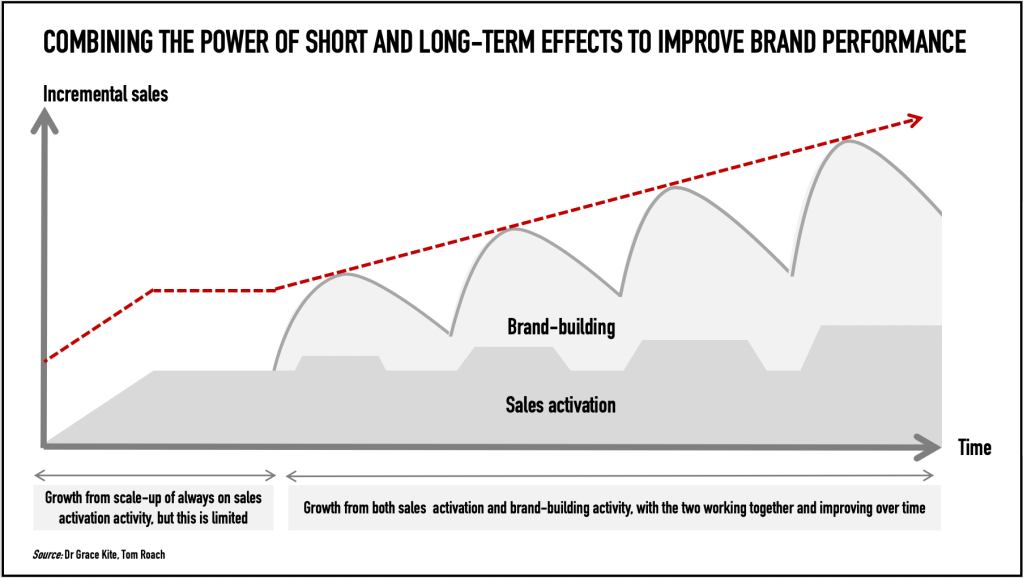

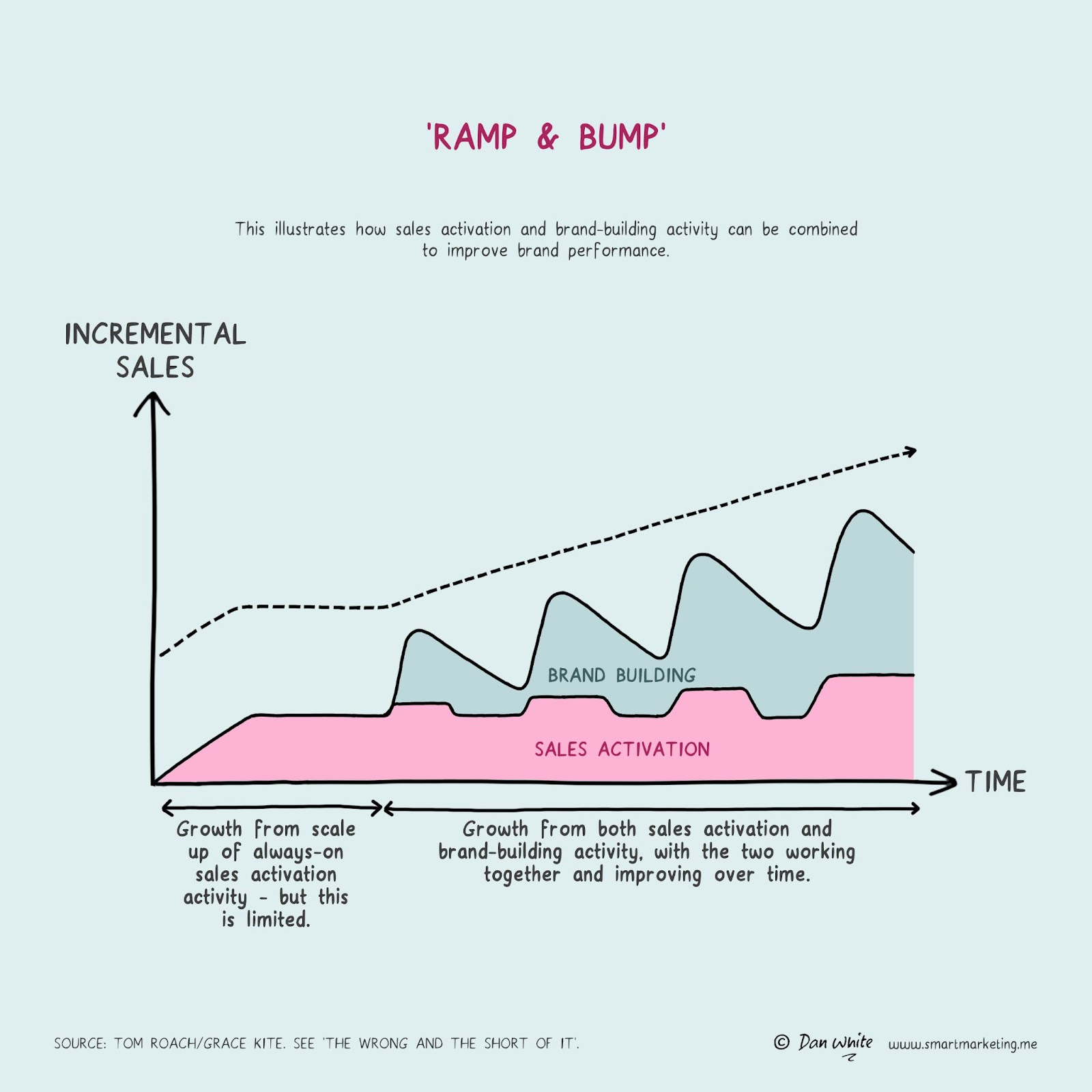

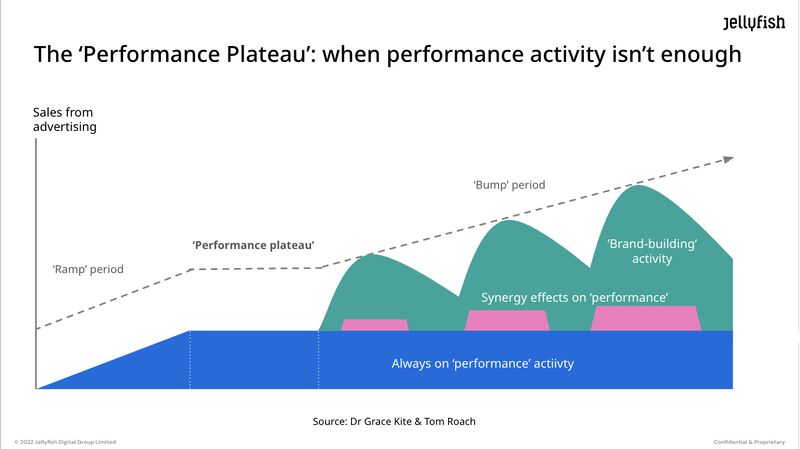

18.1.24 – PERFORMANCE PLATEAU CHART

It’s three and a half years since Dr Grace Kite and I drew this chart to illustrate the typical life stages of online born businesses, and to show the benefits of combining brand building and performance activity to help them grow.

It was based on our experiences working with brands in many categories, including Grace’s econometric modelling work. It self-consciously built on Les Binet and Peter Field’s vastly more famous and influential illustration of the two ways marketing communications work. After we published it someone called it ‘The ramp & bump chart’ which has a nice ring to it.

We’ve both used it in various posts and articles, and people often say to us it resonates with their experience and that they’ve seen it play out in the real world for their brands.

I’d love to write something about all the real world examples of brands who’ve been on a similar journey, so could I ask you a question?

Has your brand followed this path? Is it now, or was it ever, stuck on the performance plateau? Is it now growing beyond it? Can you share more about what you did to make that happen? Maybe this chart even helped you get your brand growing again?

It would be great to know.

Original Linkedin post:

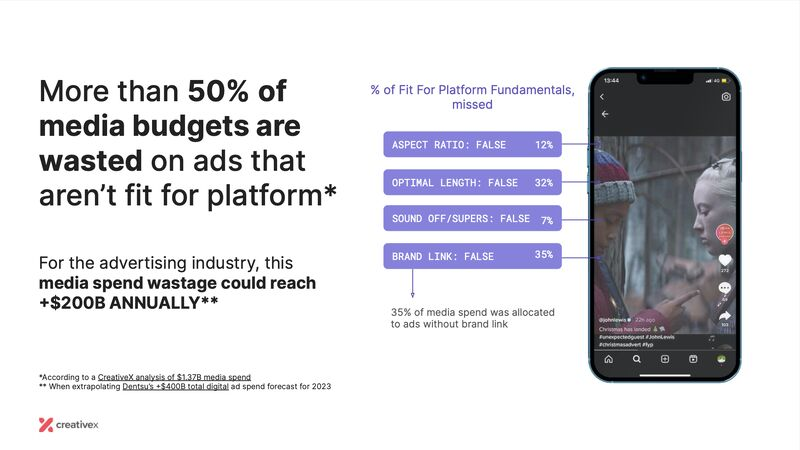

15.11.23 – 50% OF MEDIA BUDGETS GO BEHIND CREATIVE THAT ISN’T FIT FOR PLATFORM

50% of digital ad budgets go behind creative that isn’t fit for platform, say CreativeX.

Yes they would say that – they’re a data company using AI to help some of the world’s biggest brands score the creative quality of the assets they’re spending billions on.

But we all know there’s no point making beautiful ads if you’re not even getting the basics right. They say $bns are wasted from poor branding, framing, aspect ratios, length, subititling, missing messages.

We all see this kind of thing on our screens and in our feeds every day.

Getting this stuff right won’t have you jetting off to Cannes, but it will keep your CFO happy that you’re not hemorhaging cash without even knowing it.

Link to their report on the opportunity cost of poor quality creative, and how to avoid it, in comments. https://learn.creativex.com/creativex-report-waste-not-want-not

Original Linkedin post:

13.11.23 – THE US ‘VS’ UK MARKETING EFFECTIVENESS DISCUSSION

There are brilliant US marketing teams and agencies using the predominantly UK/AUS/NZ theory to get to great marketing practice (McDonald’s always comes to mind first here).

But this is rare and marketing effectiveness practice lags behind there. Mark Ritson nails the issues below.

The standard answer to the problem you hear is ‘get Americans to read Binet & Field’. Much as I’d love this to happen, this answer falls at the first hurdle. US marketers and businesses want big, simple, aspirational, super-successful examples of the path to follow, not books to read, however much we believe they should read the classics.

So this is my brief to anyone who wants to help.

The Problem

Great marketing effectiveness practice and theory is massively under-penetrated in the US. The UK/AUS/NZ work of the last 10-15 years is failing to make an impact. The leading thinkers (Byron, Binet & Field, Ritson, Nelson-Field) are less known in the US. A radical new approach is needed.

Towards a solution

Just re-skinning the existing UK/AUS/NZ approach will not work.

The answer must be homegrown to the US, not imported.

It must speak the audience’s language.

It must be big, aspirational, impactful and commercial.

It could focus on the big numbers.

It must be heavy on action and how-to, light on theory and academia.

It must avoid the semantic debates and academic squabbles common here.

Any spokespeople or experts must be from the US.

It must look forward and fully embrace digital. No nostalgia.

It shouldn’t use the word ‘effectiveness’.

The Big Idea: ‘The Trillion Dollar Opportunity’

A massive, positive, aspirational rallying cry for the potential opportunity of doing better, more impactful brand marketing.

What this could look like

A Jeff Bezos keynote at Cannes on the Trillion Dollar Opportunity. He shares the greatest advertising U-turn story ever told. Taking Amazon from being a company that thought ads were a tax on a poor product, to Amazon being one of the world’s largest, best advertisers, and itself a major advertising business. He presents it with the evangelical zeal of the convert.

Scott Galloway or Kara Swisher interview Bezos. They present the simple case behind the ‘trillion dollar opportunity’, showing that if US/Global brands did better marketing they’d benefit from their share of the trillion dollars of growth they’re currently missing out on.

A multi-year programme of content. Fronted by US thinkers and speakers, big name CEOs and CMOs. Billionaires from specific categories present their own versions of the ‘Bezos’ story (tech brands in Silicon Valley, financial brands in NYC etc).

Could include a new Cannes awards category: The Trillion Dollar Lion for the biggest commercial turnarounds and practical application of marketing effectiveness. etc etc

Budget: not a trillion dollars

Timings: review tomorrow?

Mark Ritson’s column https://www.marketingweek.com/effectiveness-ignorance-american-marketing/

Original Linkedin post:

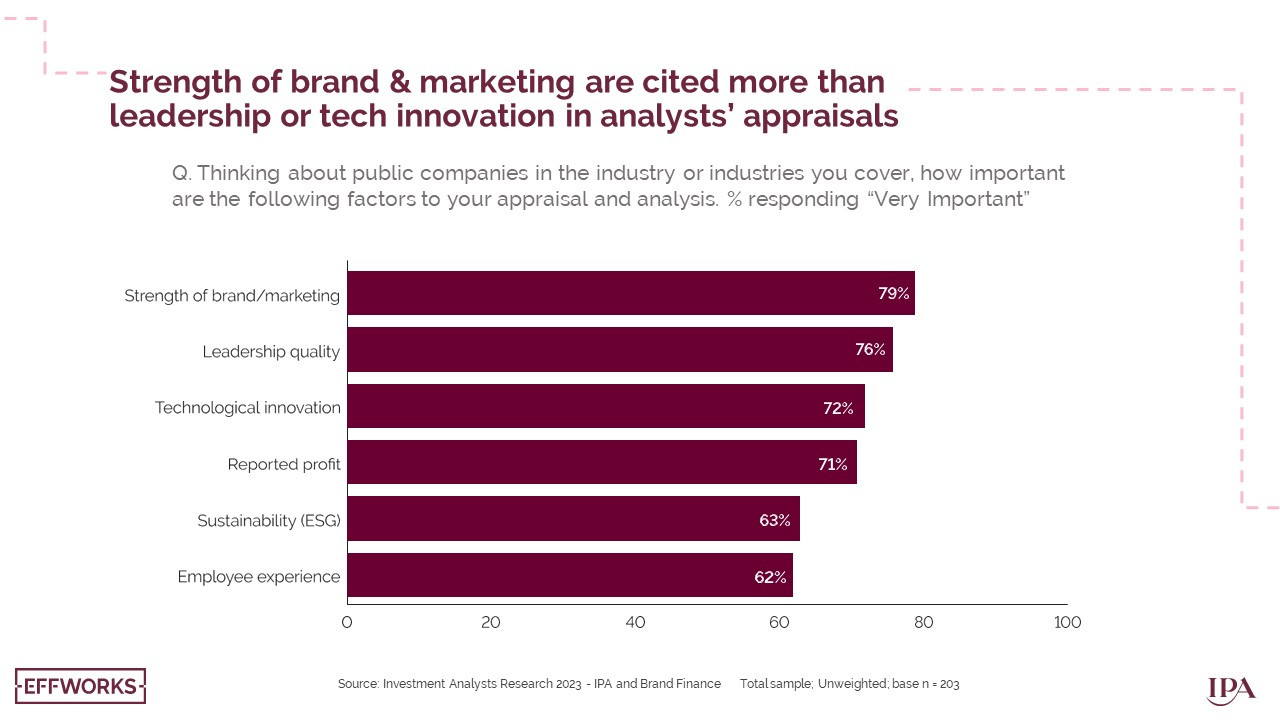

19.10.23 – BRAND INVESTMENT ACTUALLY DOES MATTER TO THE CITY

Despite what people often think, brand and marketing investment actually does matter to analysts and the City, according to a new IPA/Brand Finance survey.

“Strength of brand/marketing” is the factor most frequently cited by analysts (at 79%) when asked how they appraise and analyse the companies they cover. This is cited ahead of leadership quality (76%) and technological innovation (72%)

Some useful charts in this for anyone involved in trying to convince brand and marketing sceptics of their importance.

Original Linkedin post:

14.10.23 – WHAT’S YOUR PROBLEM, MARKETERS?

I mean, what are the REAL questions and issues that you, marketers, are dealing with right now? The ones that really matter in the day to day, the issues you’re grappling with, the things that will actually impact whether you’ll meet your targets?

I’m fairly sure it won’t be whether to focus more on differentiation or distinctiveness, what new shape your diagram of the sales funnel should be, whether brand purpose is a load of marketing BS, or whether your ratio between brand:performance should be 60:40 or 65:35.

And yet those are the kinds of topics the marketing press seems to focus on most of the time. And I should know, as I’ve written about them all in Marketing Week and my blog (links for both in comments).

But I’m beginning to think the marketing press and blogs like mine don’t actually get into a lot of the real issues marketers face.

So I’m asking here if you could share your real questions and issues below.

With Twitter in decline as a place of genuine discussion, debate and community in our industry, maybe this place could begin to replace it. Maybe people on here will be able to reply with an answer or point you in the direction you need to start to answer your question. Maybe your question will spark a new article from me (this would actually be helpful as I’ve had a bit of writer’s block recently). Or maybe our great strategy team at Jellyfish might be able to help – we’ve got a breadth and diversity of expertise spanning every possible aspect of digital marketing here that we might be able to connect you to.

So tell me, what’s your problem?

17.08.23 – LET’S MAKE BETTER ADS

Here’s a simple but important reason for us all to want to make better advertising: it helps make our industry appealing to the next generation.

Ads have changed out of all recognition since this 1986 classic. But it’s the one that made me think ads were interesting, could be intelligent, worth talking about, and that making them could be something to look into as a job about 12 years later.

There’s never been more advertising, but it’s never been more invisible.

We’ve never had smarter technology to make it with, but ads have never been dumber.

Let’s make better ads people.

Guardian Points of View: https://youtu.be/_SsccRkLLzU

Original LinkedIn post: https://www.linkedin.com/posts/tom-roach-5b468026_the-guardians-1986-points-of-view-advert-activity-7098033312505425920-p8U9?utm_source=share&utm_medium=member_desktop

21.12.22 – MY ‘CONTENT’ FROM 2022

The world is over-supplied with ‘content’, and this is as true of the marketing world as any other. So when I write stuff I’m really conscious of not adding too much to the internet’s infinite content shelf (or its infinite content bin depending on your point of view). Most years I add about 10,000-12,000 words to it, in about 5-6 posts and articles.

2021 was about new beginnings at Jellyfish, reviewing the ubiquitous sales funnel, and why what won’t change is just as important as what will.

2022’s batch was about why advertising will never die, why ROAS is a problem, and how to help brands get off the Performance Plateau.

Here they are:

Performance plateau: https://lnkd.in/ebxU5Ysm

ROAS: https://lnkd.in/eJfEicka

ROI: https://lnkd.in/eQGsN_Vz

Advertising won’t die: https://lnkd.in/eRFbrE8n

First 12 months at Jellyfish: https://lnkd.in/eJiaS3MJ

Most of these start out as Marketing Week articles and then end up here: thetomroach.com.

Thanks for reading.